Hotel Loan Market Update November 2025: Rates Falling, Bank Loans & Construction Costs

Minibar and Loan Market Update from Bridge

Welcome to the November Minibar + Loan Market Update — your quick shot of what’s moving hotel financing this month. My name is Rohit Mathur (and again I typed this entire newsletter, not chatgpt).

I’m the co-founder and CEO of Bridge, a direct lender and marketplace for hotel loans. Before founding Bridge, I spent 10+ years at Citi in capital markets.

This is month 2 of our minibar and loan market update.

🎯 TLDR: What’s Moving in the Loan Market:

- Rates – down again, what does that really mean for my deal?

- “Costs are high right now but maybe I should still start my project”. Also, do costs ever come down?

- Two things can be true at once: Banks are offering increasingly competitive rates, even as cracks begin to show in commercial real estate portfolio performance.

🏨 Key Takeaway from the Lodging Conference:

I asked the Harry Javer, CEO of Lodging Conference to give me his take-away for this update. He said:

The key theme at the conference was Uncertainty. But seasoned developers and operators know that historically, volatile markets create the best opportunities.

At Bridge, we completely agree with this statement. Uncertainty still exists — absolutely — but that’s exactly what creates opportunity. The uncertainty curtails institutional development- that means less competition for marquee flags, GCs, lenders etc.

This creates opportunities for non-institutional hotel owners who are developing a few hotels at once.

📉 3 Observations from October:

1. Rates – down again, what does that really mean for my deal?

- We have now seen our second rate cut of the year - the FED cut rates .25% in October

- As I write this, the rates that matter to you are:

- Prime Rate: 7.00% [down from 7.5% at end of Q1 2025]

- SOFR: 4.04% [down from 4.41% at end of Q1 2025]

- 5 year Treasury Rate: 3.69% [down from 3.98% at end of Q1 2025]

- View Interest Live Rates 👉 HERE

- Also embedded in the most recent commentary was the indication that there may not be further cuts in 2025 (although the market is still expecting another 0.25% cut in 2025)

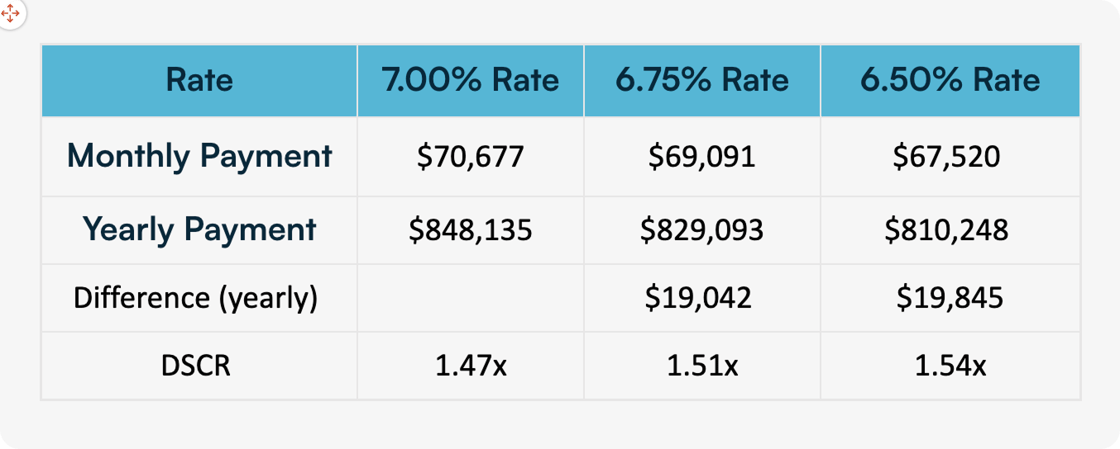

- As an industry, we always want to ensure that we are getting the best rates for our deals – we often negotiate every 10 – 20 bps rate reduction on a deal to ensure that spreads work, but what does that mean for our deals?

- Here is a simple table I created to show the difference for the same deal on the monthly payment and DSCR with a 0.25% reduction and 0.50% reduction in rates. Assumptions are all the same for each scenario–

- $10.0 million loan | 5-year maturity | 25 year amortization | $1.25 million NOI | Fixed rate

- Do lower rates help – Yes, absolutely they do. But lower rates also typically signal higher expectations for prices and acquisition.

- My two cents: We don’t expect a massive move in rates, so if your project underwrites under these rates, don’t want for 0.25% or even 0.50% - its very hard to time the interest rate market, you’re better off getting your deal done!

2. “Costs are high right now but maybe I should still start my project”. Also, do costs ever come down?

- We’re almost through 2025 and here is how discussions have gone this year:

- January 2025 (ALIS Conference) – Optimism. Developers were expecting rates to go down, costs were high but sponsors were expecting a good year to develop new projects

- March / April 2025 (AAHOA + Hunter Conference) – Fear. Tariffs created uncertainty, a reduction in travel from certain countries (such as Canada), RevPar was flat to down for the year, rates stayed higher. Developers felt that costs were too high to develop new projects

- Summer 2025 – Even more fear (and maybe some loathing!). High prices and uncertainty continued through the summer with most developers siting on the sidelines vs. starting a new development. Even acquisition activity was diminished.

- October 2025 (Lodging Conference) – Acceptance. Best characterized by: “I think I’m just going to start my project, because costs aren’t really coming down and I’ve been waiting for over 12 months now”

- The new sentiment that we felt at Lodging is in line with what we heard from developers, brands and industry experts – the cost of not starting your project continues to go up.

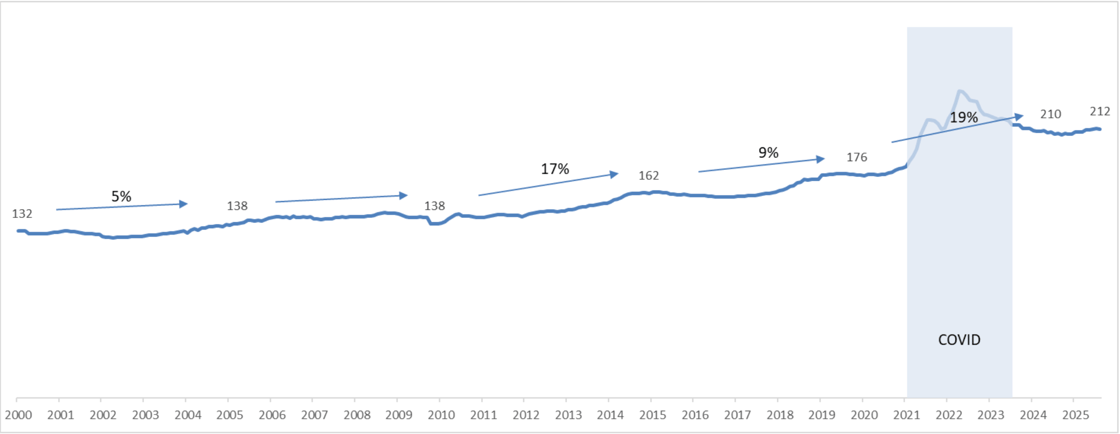

- Here is a graph to drive home that point: Index of Lumber and Wood Products Prices over time. Outside of COVID which created supply chain challenges - prices have only increased over the years.

Chart of the Month

- The sentiment in Q4 has changed to an acknowledgement that prices are high and updated underwriting to see how deals can still pencil. This is especially true if you’ve been sitting on vacant land or (even worse) you have a land loan and you haven’t started construction… the cost of not starting your project is actually only growing higher.

3. Two things can be true at once: Banks are offering increasingly competitive rates, even as cracks begin to show in commercial real estate portfolio performance.

- For over 2 years, we’ve been hearing about the CRE maturity wall, extend and pretend by banks, challenges in bank CRE portfolios etc. (the NY FED even wrote a paper about it in October 2025 Link

- During that time we’ve seen banks pull back significantly from CRE lending but more recently, come back into CRE lending (atleast for acquisitions and refinancings). We recently saw one of the most competitive term sheets we’ve received in the past 3 months:

- Refinance - Conventional bank at an all in yield of 6.25% - that’s the lowest we’ve seen on a 5 year conventional loan. For reference, 7.25% seemed market just over the summer (rates and spreads have come down for certain projects)

- Last month, Zions Bancorporation's California Bank & Trust division disclosed a significant charge-off ($50.0 million charge off) related to a single borrower, which intensified worries about credit quality and led to a drop in regional bank stock values

- While this was fraud and misrepresentation related – the overall concerns about the industry were heightened and the significant sell off demonstrated the investor fear regarding portfolio quality

- Why should this matter to you? If CRE credit concerns are heightened, banks will be embroiled in work out / clean up and it will make new deals more challenging

About Bridge

We are the first fintech focused on Hospitality loans and partners with Hilton, AAHOA, Choice, Red Roof and others. We’ve closed and funded $350.0 million+ in loans in 2025 (Our 1st full year of Hotel Lending) and we only have one goal:

🎯 Simplifying access to competitive financing for your hotel loan.

💡 Tools to Help You Get Funded

- Five-click Pro Forma Generator - Link

- C-PACE Calculator – determine if your project is CPACE eligible and how much you can get - Link

- DSCR Calculator – does your deal cash flow - Link

- Free Offering Memo - Have we generated an Offering Memorandum for you yet? We’ve built an OM for over 150 other projects in the past 3 months- get one now Link

- Data Room – the cost of not having everything in one place is that lenders move on to the next deal – we’ve built a hospitality focused deal room (Want to see it? Just reply to this email and I'll give you a live demo)

Where will Bridge be in November?

- 2025 AAHOA Southwest Hotel Owners Conference and Trade Show – we are sponsoring!

- 2025 AAHOA CHLA North Pacific Hotel Owners Conference and Trade Show

Bridge Minibar Update 🍸 🍺

- Stocking up for the winter – not as much travel and everyone will be in the office!